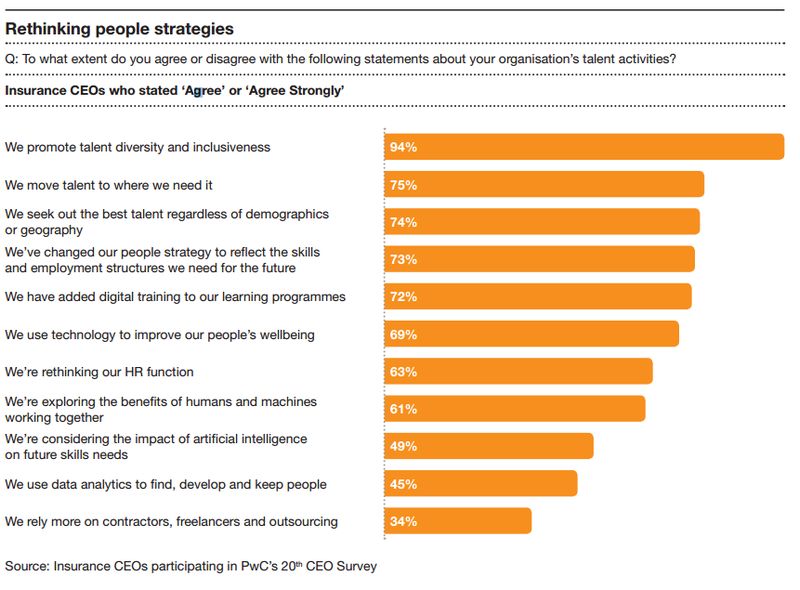

However, insurance CEOs are also among the readiest to embrace disruptive change: 67% see creativity and innovation as very important to their organisations, while 61% are exploring the benefits of humans and machines working together.

The latest edition of PwC Global CEO Survey, now at its 20th edition, gathers the views of nearly 1,400 CEOs on the impact that globalisation and technological change have on growth, talent, trust and society. The findings for the insurance industry are based on the views of 95 insurance CEOs in 39 countries who participated in the survey.

Optimism: Over a third of insurance CEOs, very confident they can achieve revenue growth over the next year

Despite soft premium rates, low interest rates, and subdued economic growth in many developed markets, insurance CEOs are optimistic about their own companies' prospects. Over a third (35%) are very confident that they can achieve revenue growth over the next year (compared to 38% last year) and more than 80% are at least somewhat confident, shows the report.

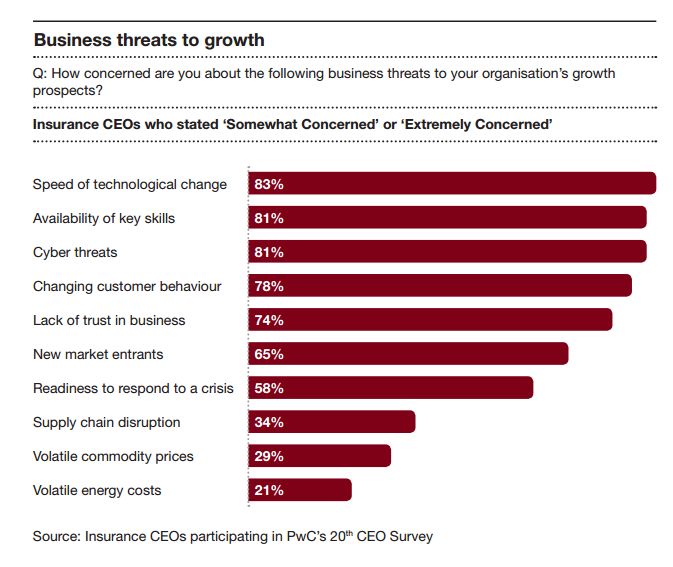

However, insurance CEOs are acutely aware of the disruption and change facing their industry, the transformational impact of which is now evident in areas ranging from robo-advice to pay-as-you-go and sensor-based coverage. Concerns over regulation, the pace of technological change, shifting customer behaviour, and competition from new market entrants have continued to rise from their already high levels. When the impact is put together, no other sector is facing as much disruption in these four areas.

The insurance companies seem ready to face these challenges, being ready to embrace the new possibilities: 67% of industry leaders see creativity and innovation as very important to their organisations, ahead of other financial services (FS) sectors. Insurance CEOs are also ahead of the curve in exploring the benefits of humans and machines working together (61%) and considering the impact of artificial intelligence (AI) on future skills needs (49%).

Regulation remains a key concern

According to PwC's findings, the cost and disruption of regulation continue to be the insurance industry leaders' paramount concern. 95% of them are at least somewhat concerned about the potential impact of over-regulation on their growth prospects, and 67% are very concerned, more than any other sector in the CEO Survey, including banking and capital markets.

The pace of technological change and related shifts in customer behaviour are prominent on insurance CEOs' list of business threats to growth, though they also represent huge opportunities at a time when customer intelligence is emerging as of the main predictors of profitability and growth. 28% of insurance CEOs believe technology will completely reshape competition in the industry over the next five years, and another 58% say it will have a significant impact.

InsurTech: Threats and opportunities for insurers

Cutting edge customer interaction and data analytics have enabled InsurTech businesses to set the pace in the marketplace, especially in relation to customer intelligence. Insurance CEOs' concerns about competition from new entrants are notably higher than other FS sectors facing similar incursions from FinTech firms. The threat has been heightened by a fivefold increase in annual investments in InsurTech start-ups in the three years up to 2016, with cumulative funding since 2010 reaching $3.4 billion.

However, according to PwC's report, rather than being just a threat, the growing presence of InsurTech companies could open up valuable opportunities for insurers and enable them to make the leap from incremental to breakthrough innovation. InsurTech partnerships can help insurers:

- improve their processes and thereby strengthen efficiency and reduce costs;

- improve their analysis of the huge amounts of data at their disposal, which can lead to better customer understanding, higher win-rates, and more informed underwriting.

Reducing costs by greater automation of routine tasks

Productivity, price monitoring, tax efficiency and curbing claims leakage continue to be vital strategies for reducing costs. However, one other important trend is a greater automation of routine tasks, which can not only reduce costs and improve efficiency, but also free up staff to devote more time to customers and higher value growth areas such as cyber risk insurance.

According to PwC's report, promising technologically enabled solutions include:

- Using machine learning, advanced analytics, and sensor technologies to target clients, evaluate their needs, develop customised solutions, and price risk in real-time. The benefits include more focused sales and marketing investments, and more favourable outcomes for policyholders.

- Automation and AI are already cutting costs by speeding up routine underwriting and providing a more informed basis for pricing and loss evaluation. The emerging opportunities range from equipment sensors to cognitive computing as insurance moves from compensating client losses to anticipating what will happen and when (predictive analytics) and proactively shaping the outcome (prescriptive analytics).

- Robotics is rapidly reshaping the back office and reducing costs. Prominent examples include finance, where previously disjointed systems are being connected through simple new software. Advantages include allowing data to flow more easily around the business without the need for endless re-keying.

With a hybrid human and machine workforce set to be a key element of the fit for growth model, many insurance CEOs are keen to explore the benefits of humans and machines working together. Moreover, diversity and inclusion are moving up the agenda as insurance CEOs look to broaden their talent pool and bring in the fresh ideas and experiences needed to foster innovation. Ninety four per cent of insurance CEOs are keen to promote talent diversity and inclusiveness, more than those in any other industry PwC surveyed.

The complete key findings in the insurance industry can be accessed here.

7562 views